ax Audit in India Explained: Who Needs It, Penalties, Due Dates & Compliance Tips

TL;DR A tax audit under Section 44AB of the Income Tax Act is mandatory for eligible businesses and professionals crossing prescribed turnover or income thresholds. Non-compliance can result in penalties, scrutiny notices, and financial reporting issues. Businesses that maintain accurate bookkeeping, GST reconciliation, and organized documentation throughout the year significantly reduce audit risks. What Is a Tax Audit? A tax audit is an examination of a taxpayer’s financial records conducted by a Chartered Accountant to verify whether income, deductions, expenses, and compliance records are correctly maintained according to the Income Tax Act. The objective of a tax audit is to: Ensure accurate income reporting Verify tax compliance Reduce tax evasion Improve financial transparency Standardize reporting practices For businesses in India, tax audits have become increasingly important due to: GST data integration AIS and TIS reporting systems Digital payment tracking Advanced income tax analytics Automated discrepancy detection Today, mismatches between GST returns, bank transactions, and income tax filings can quickly trigger notices or scrutiny. What Is Section 44AB of the Income Tax Act? Section 44AB: Mandatory Tax Audit for Eligible Businesses and Professionals\text{Section 44AB: Mandatory Tax Audit for Eligible Businesses and Professionals}Section 44AB: Mandatory Tax Audit for Eligible Businesses and Professionals Section 44AB governs tax audit applicability in India. It mandates certain businesses and professionals to get their accounts audited by a Chartered Accountant and submit the audit report before the prescribed due date. The audit report is typically filed using: Form 3CA / 3CB Form 3CD These forms contain detailed disclosures related to: Turnover Expenses GST compliance Related-party transactions TDS compliance Depreciation Cash transactions Who Needs a Tax Audit in India? 🔍 1. Businesses Businesses are generally required to undergo tax audit if turnover exceeds prescribed limits under Section 44AB. 2. Professionals Professionals such as: Doctors Architects Consultants Chartered Accountants Freelancers Lawyers may require tax audit based on gross receipts thresholds. 3. Presumptive Taxation Cases Businesses or professionals opting for presumptive taxation under: Section 44AD Section 44ADA Section 44AE may also become liable for audit under specific circumstances, especially when declaring lower profits than prescribed norms. This is one of the most misunderstood areas among small businesses and freelancers. Tax Audit Turnover Limits for FY 2025–26 📊 Category Tax Audit Applicability Business Applicable if turnover crosses prescribed limits under Section 44AB Professionals Applicable based on gross receipt threshold Presumptive Taxation Audit applicable under certain lower-profit declarations Businesses should always consult a qualified Chartered Accountant because applicability can vary based on: Digital transaction percentage Nature of business Presumptive taxation selection Profit reporting structure Important Tax Audit Due Dates 🗓️ Missing due dates is one of the biggest compliance mistakes businesses make. Typically, businesses requiring tax audit must: Complete books of accounts Finalize financial statements Conduct audit File audit report Submit income tax return well before statutory deadlines. Late preparation creates: Reporting errors Reconciliation mismatches Documentation gaps Filing pressure Businesses operating in Mumbai often face additional operational complexity due to high transaction volumes and multi-state GST activity. Documents Required for Tax Audit 📂 Maintaining organized documentation simplifies the audit process significantly. Common Documents Include: Sales invoices Purchase records Bank statements GST returns TDS returns Expense vouchers Payroll records Loan statements Fixed asset register Previous audit reports Additional Supporting Records E-invoices Vendor reconciliations Inventory reports Cash book Profit and loss statements Balance sheet schedules Poor documentation is one of the leading causes of audit delays. Common Mistakes Businesses Make During Tax Audit 1. GST Reconciliation Errors Many businesses fail to reconcile: GSTR-1 GSTR-3B E-way bills Books of accounts This creates discrepancies that may attract notices from both GST and Income Tax departments. 2. Improper Expense Claims Businesses often claim: Unsupported expenses Personal expenses as business expenses Incorrect depreciation Unverified vendor payments These claims increase audit exposure significantly. 3. Cash Transaction Violations High-value cash transactions remain a major compliance risk. Improper handling of: Cash receipts Cash expenses Related-party cash dealings can trigger scrutiny under multiple provisions of the Income Tax Act. 4. Ignoring TDS Compliance Mismatch in TDS deduction or delayed filing creates cascading compliance issues. Businesses must reconcile: TDS returns Vendor payments Form 26AS AIS reporting regularly throughout the financial year. 5. Last-Minute Accounting One of the biggest operational mistakes is postponing bookkeeping until year-end. This usually results in: Incomplete records Missed entries Incorrect reconciliations Filing stress Continuous accounting discipline reduces audit complications dramatically. Penalties for Non-Compliance Failure to comply with tax audit requirements may result in penalties under the Income Tax Act. Consequences may include: Monetary penalties Increased scrutiny risk Delayed refunds Compliance notices Disallowance of expenses Litigation exposure Businesses should avoid treating tax audit as a last-minute compliance exercise. Practical Tax Audit Compliance Tips ✅ Maintain Monthly Bookkeeping Regular accounting reduces year-end pressure and improves reporting accuracy. Reconcile GST Every Month Monthly GST reconciliation helps detect mismatches early. Separate Personal and Business Transactions Mixing transactions creates audit complications and weakens financial transparency. Digitize Financial Records Cloud-based accounting systems improve: Record accessibility Audit readiness Reporting accuracy Compliance tracking Work With a Professional CA Firm A structured Chartered Accountant firm can help businesses: Maintain proper records Ensure statutory compliance Reduce tax exposure Respond to notices Improve audit preparedness How CA Arihant Lodha Helps Businesses Stay Audit-Ready CA Arihant Lodha assists startups, SMEs, professionals, and established businesses with: Tax audit support Accounting and bookkeeping GST reconciliation Income tax compliance Financial reporting Audit preparedness Business compliance management The firm focuses on proactive compliance systems that help businesses reduce risks and maintain accurate financial records throughout the year. Final Thoughts Tax audit compliance is no longer just a statutory requirement. It is now a critical part of financial governance and business credibility. Businesses that maintain clean books, timely reconciliations, and structured compliance systems: reduce scrutiny risks, improve operational clarity, strengthen financial reporting, and avoid unnecessary penalties. As regulatory systems become increasingly data-driven in 2026, businesses must move from reactive compliance to proactive audit readiness. Partnering with an experienced Chartered Accountant firm can make that transition significantly easier and more reliable. FAQ SECTION 1. Who needs a tax audit in India? Businesses and professionals crossing prescribed turnover or receipt limits under Section 44AB may

Why Small Businesses in Mumbai Are Switching to Outsourced Accounting & Bookkeeping Services 1

TL;DR Mumbai small businesses are outsourcing accounting to improve compliance and operational efficiency Outsourced bookkeeping reduces errors and improves reporting accuracy Mumbai businesses gain access to professional accounting expertise without building large internal teams GST, TDS, and tax compliance management become more streamlined Cloud accounting tools are driving the outsourcing trend in 2026 Introduction Mumbai small business ecosystem is evolving rapidly. From startups and agencies to retailers and e-commerce brands, businesses today operate in an environment where: Compliance requirements are stricter GST scrutiny is increasing Financial reporting expectations are higher Operational efficiency directly affects profitability Many business owners initially attempt to manage accounting internally. But as operations grow, they face recurring problems: Delayed bookkeeping GST mismatches Incomplete financial records Poor cash flow tracking Filing errors This is one of the biggest reasons why businesses across Mumbai are increasingly shifting toward outsourced accounting and bookkeeping services. In 2026, outsourced finance support is no longer viewed as an optional convenience. For many SMEs, it has become a strategic business decision. Why Traditional Accounting Models Are Failing SMEs Small businesses often rely on: One internal accountant Manual spreadsheets Delayed reconciliation processes This creates several operational risks. Common problems include: Inconsistent bookkeeping entries GST return mismatches Vendor reconciliation issues Missing invoices Poor audit preparedness Lack of monthly reporting discipline As transaction volumes increase, these problems multiply quickly. Most SMEs realize the issue only when: ❌ Tax notices arrive ❌ Cash flow problems appear ❌ Investors ask for clean financial statements ❌ GST scrutiny begins What Are Outsourced Accounting & Bookkeeping Services? Outsourced accounting means delegating financial management activities to professional accounting experts outside the company. These services may include: Bookkeeping GST accounting Bank reconciliation Financial reporting TDS management Payroll accounting Tax filing support MIS reporting Instead of building a large in-house finance team, businesses work with specialized professionals using digital accounting systems. Top Reasons Mumbai Businesses Are Outsourcing Accounting 1. Better Compliance Management One of the biggest reasons businesses outsource accounting is compliance accuracy. In 2026, businesses must handle: GST returns TDS filings ROC compliance Income tax documentation E-invoicing requirements Even small errors can trigger: Notices Penalties Input tax credit issues Professional accounting firms maintain structured compliance workflows that reduce these risks significantly. 2. Access to Experienced Financial Expertise Hiring experienced finance professionals internally is difficult for many SMEs. Outsourced accounting gives businesses access to: ✔ Qualified accountants ✔ GST specialists ✔ Tax professionals ✔ Financial reporting expertise This improves: Reporting quality Tax accuracy Financial planning 3. Improved Financial Visibility Many small businesses struggle because owners lack real-time financial visibility. Outsourced bookkeeping helps businesses monitor: Cash flow Receivables Payables Tax liabilities Profitability trends Better visibility leads to better business decisions. 4. More Focus on Core Business Operations Business owners should focus on: Sales Growth Customer acquisition Operations Not chasing invoice entries or correcting reconciliation mistakes. Outsourcing accounting reduces administrative burden and allows founders to focus on scaling the business. 5. Scalability & Operational Flexibility As businesses grow: Transaction volumes increase Compliance becomes more complex Financial reporting expectations rise Outsourced accounting systems scale more efficiently compared to fragmented internal processes. This becomes especially important for: E-commerce businesses Agencies Multi-location businesses Growing startups Common Accounting Problems SMEs Face Problem Business Impact Delayed bookkeeping Poor financial visibility GST mismatches Input tax credit loss Missing invoices Audit complications Incorrect reconciliation Cash flow confusion Weak reporting Poor decision-making Manual accounting Increased human errors What Services Are Usually Outsourced? Most businesses outsource a combination of: Bookkeeping Daily transaction recording and ledger maintenance. GST Compliance GST returns, reconciliation, and ITC tracking. Payroll Accounting Salary processing and statutory deductions. MIS Reporting Monthly business performance reporting. Bank Reconciliation Matching transactions and identifying discrepancies. Vendor & Receivable Tracking Managing payment cycles efficiently. Cloud Accounting & Digital Transformation in 2026 Cloud accounting platforms have accelerated accounting outsourcing across India. Businesses now use: Real-time dashboards Automated invoicing Cloud document sharing Digital reconciliation systems Benefits include: ✔ Faster reporting ✔ Remote accessibility ✔ Reduced paperwork ✔ Better collaboration Digital accounting ecosystems are now standard for modern SMEs. How Outsourced Bookkeeping Helps with GST & Tax Compliance GST compliance has become increasingly data-driven. Authorities now monitor: Invoice matching Return consistency Vendor compliance E-way bill reconciliation Outsourced accounting teams help businesses: Maintain clean records Avoid filing mismatches Track GST liabilities properly Improve audit readiness This significantly reduces compliance risks. Industries Benefiting Most from Outsourced Accounting E-commerce Businesses High transaction volumes require structured bookkeeping. Agencies & Service Firms Project-based billing needs organized accounting systems. Retail Businesses Inventory-linked accounting becomes easier with professional systems. Startups Investor reporting and compliance become more manageable. Professional Services Consultants and service firms benefit from structured financial tracking. Mistakes Businesses Make While Choosing Accounting Partners 1. Choosing Only Based on Low Cost Low-quality bookkeeping often creates expensive compliance problems later. 2. Ignoring Industry Experience Different industries require different accounting workflows. 3. Lack of Reporting Systems Many providers record transactions but fail to deliver actionable insights. 4. Weak Communication Processes Delayed responses create compliance bottlenecks. Why Professional CA Support Matters Accounting is no longer just data entry. Modern businesses need: Compliance expertise Financial reporting clarity Tax planning support Scalable accounting systems Professional CA firms provide strategic financial support that goes beyond bookkeeping. How CA Arihant Lodha Supports Mumbai Businesses CA Arihant Lodha assists SMEs and startups with: Accounting & bookkeeping support GST compliance management Financial reporting Tax advisory Business compliance assistance Startup financial structuring Conclusion Mumbai businesses are shifting toward outsourced accounting because modern compliance and financial management require specialized expertise. The transition is driven by: Increasing GST complexity Demand for accurate reporting Need for operational efficiency Digital accounting adoption Businesses that maintain organized accounting systems gain: ✔ Better compliance ✔ Stronger financial control ✔ Improved scalability ✔ Faster decision-making In 2026, outsourced accounting is not just an operational support function — it is a competitive advantage. CTA Need professional accounting and bookkeeping support for your business in Mumbai? Consult CA Arihant Lodha for structured accounting, GST compliance, and financial management solutions tailored for startups and

LLP vs Private Limited Company in India: Which Business Structure Is Better in 2026?

TL;DR LLPs are simpler and cheaper to maintain Private Limited Companies are better for funding and scalability Startups seeking investors usually prefer Pvt Ltd structures LLPs work well for professionals, agencies, and family businesses Compliance, taxation, and long-term business goals should guide the decision Introduction Choosing the right business structure is one of the most important decisions entrepreneurs make. And in 2026, the decision matters even more because: Compliance systems are becoming stricter Investors expect structured governance Tax scrutiny has increased Startup ecosystems are more competitive Two of the most popular business structures in India are: Limited Liability Partnership (LLP) Private Limited Company (Pvt Ltd) Both provide limited liability protection, but they differ significantly in: Compliance Taxation Fundraising capability Ownership flexibility Scalability This guide explains the practical differences so founders and SMEs can choose the right structure strategically. What is an LLP? A Limited Liability Partnership (LLP) combines features of: Partnerships Corporate entities An LLP offers: ✔ Limited liability protection✔ Lower compliance burden✔ Operational flexibility LLPs are governed under the Limited Liability Partnership Act, 2008. LLPs are commonly preferred by: Consultants CA firms Agencies Service providers Family-run businesses What is a Private Limited Company? A Private Limited Company is a separate legal entity governed under the Companies Act, 2013. It offers: ✔ Separate corporate identity✔ Shareholding structure✔ Better investor confidence✔ Easier fundraising opportunities Private Limited Companies are highly preferred by: Tech startups Venture-backed businesses Fast-scaling companies E-commerce brands LLP vs Private Limited Company: Key Differences Factor LLP Private Limited Company Governing Law LLP Act Companies Act Ownership Partners Shareholders Liability Limited Limited Compliance Lower Higher Audit Requirement Conditional Mandatory in many cases Funding Capability Limited High ESOPs Not Available Available Investor Preference Low High Scalability Moderate High Annual Compliance Cost Lower Higher 1. Ownership Structure LLP Managed by partners Flexible operational structure Partnership agreement defines roles Private Limited Managed by directors Ownership divided into shares Stronger governance framework Best for: LLP → Closely managed businesses Pvt Ltd → Structured scaling businesses 2. Compliance Requirements This is where most founders underestimate the difference. LLP Compliance Typically includes: Annual Return Statement of Accounts Income Tax Return Private Limited Compliance Includes: Board meetings ROC filings Financial statements Annual return filings Statutory audit requirements Important: Private Limited Companies generally have: ❌ Higher compliance burden❌ Higher professional costs But they also offer: ✔ Better credibility✔ Investor readiness 3. Taxation Comparison LLP Taxation Flat income tax rate Dividend distribution flexibility No dividend tax implications like companies Private Limited Taxation Corporate tax applies Dividend distribution rules applicable Better tax structuring possibilities for scaling businesses In practice: LLPs often work better for: Moderate-profit service firms Private Limited Companies work better for: Reinvestment-heavy growth businesses 4. Funding & Investment Potential This is one of the biggest differentiators. LLP Challenges: Cannot issue shares Limited investor flexibility Venture capital firms rarely prefer LLPs Private Limited Company Advantages: ✔ Equity issuance possible✔ ESOPs possible✔ Preferred by VCs and angel investors If your goal is fundraising: 👉 Private Limited Company is usually the stronger option. 5. Scalability & Expansion LLP Suitable for: Stable businesses Professional practices Regional operations Private Limited Suitable for: National expansion Investor-backed growth Multi-founder scaling International business expansion 6. Credibility & Brand Perception Many vendors, investors, and enterprise clients perceive: Private Limited Companies as more structured and scalable LLPs as more suitable for smaller professional businesses This perception affects: Funding Partnerships Enterprise contracts Which Structure is Better for Startups? Choose LLP if: ✔ You want lower compliance✔ You run a professional service business✔ External funding is not a priority✔ You want operational flexibility Choose Private Limited if: ✔ You plan to raise investment✔ You want rapid scaling✔ You need ESOPs✔ You expect multiple shareholders Which Structure is Better for Small Businesses? For many SMEs and local businesses: 👉 LLP can be more cost-effective. For growth-focused businesses: 👉 Private Limited often becomes the smarter long-term structure. Compliance Cost Comparison in 2026 Expense Area LLP Pvt Ltd Registration Cost Lower Higher Annual Filing Lower Higher Audit Cost Conditional More Frequent Secretarial Compliance Minimal Significant Common Mistakes Entrepreneurs Make 1. Choosing Structure Only Based on Cost Cheap registration today can create scaling limitations later. 2. Ignoring Future Funding Goals Businesses planning investment should avoid structural limitations early. 3. Underestimating Compliance Many founders fail to budget for ongoing ROC and tax compliance. 4. Copying Competitors Blindly Your business structure should match: Revenue model Growth goals Investor expectations Tax planning strategy How to Choose the Right Business Structure Ask these questions: Will you raise funding? How fast do you plan to scale? Do you need ESOPs? How much compliance can you manage? Is tax efficiency your priority? The answers usually clarify the right structure. Why Professional CA Guidance Matters Business registration decisions affect: Tax planning Investor readiness Compliance burden Future restructuring costs Professional CA firms help entrepreneurs: ✔ Choose the correct structure✔ Handle registration smoothly✔ Maintain ROC & GST compliance✔ Avoid costly legal mistakes Why CA Arihant Lodha is a Strong Business Registration Partner CA Arihant Lodha assists startups and SMEs with: LLP registration Private Limited Company incorporation GST registration ROC compliance Startup advisory Tax planning Conclusion There is no universally “best” business structure. The right choice depends on: Your growth vision Funding plans Compliance capacity Tax strategy In general: ✅ LLP → Better for operational simplicity✅ Private Limited → Better for aggressive scaling and investment Choosing correctly in the beginning prevents expensive restructuring later. CTA Need help deciding between LLP and Private Limited Company registration? Consult CA Arihant Lodha for expert startup registration, GST, and compliance advisory in Mumbai. FAQ SECTION 1. Which is better LLP or Private Limited Company? It depends on your goals. LLPs are simpler and cost-effective, while Private Limited Companies are better for scaling and investment. 2. Can LLP raise funding from investors? LLPs face limitations in raising equity funding because they cannot issue shares like companies. 3. Is LLP good for startups? Yes, especially for bootstrapped service businesses with lower compliance needs. 4. Which structure has lower compliance

GST Registration vs GST Compliance: What Mumbai Businesses Often Get Wrong

TL;DR gst registration is only the first step—not full compliance Many Mumbai businesses mistakenly believe registration alone is sufficient GST compliance includes filing, reconciliation, invoicing, and reporting Errors can trigger notices, penalties, and audits Professional GST management significantly reduces compliance risks Introduction Many businesses celebrate after receiving their GST number. But that’s where the real work actually begins. One of the biggest misconceptions among startups and SMEs in Mumbai is believing that gst registration equals GST compliance. It doesn’t. In 2026, GST systems are more automated, interconnected, and scrutiny-driven than ever before. Businesses that fail to maintain ongoing compliance face: Penalties Input Tax Credit (ITC) reversals GST notices Departmental scrutiny This guide explains the crucial difference between GST registration and GST compliance—and the mistakes businesses must avoid. Understanding GST Registration GST registration is the process of obtaining a GST Identification Number (GSTIN) from the government. Businesses typically require registration if: Turnover exceeds threshold limits They sell interstate They operate through e-commerce platforms They fall under mandatory GST categories Registration legally enables businesses to: ✔ Collect GST✔ Claim Input Tax Credit✔ Issue GST invoices However: Registration alone does not mean you are compliant. What is GST Compliance? GST compliance refers to the ongoing responsibilities businesses must fulfill after registration. This includes: Filing GST returns Paying GST on time Reconciling invoices Maintaining proper records Following e-invoicing rules Reporting accurate turnover GST compliance is continuous—not one-time. GST Registration vs GST Compliance: Key Differences Factor GST Registration GST Compliance Nature One-time process Ongoing process Purpose Obtain GSTIN Maintain legal compliance Timeline Initial setup Monthly/Quarterly/Annual Includes Filing? No Yes Includes Reconciliation? No Yes Risk if Ignored Cannot legally collect GST Penalties & notices Common GST Mistakes Mumbai Businesses Make 1. Assuming Registration is Enough Many businesses register under GST and then: Skip return filing Ignore reconciliations Delay tax payments This quickly creates compliance issues. 2. Ignoring Monthly & Quarterly Filings Businesses often miss: GSTR-1 GSTR-3B Annual returns Late filing results in: Interest Late fees Compliance risk scores 3. Incorrect ITC Claims Input Tax Credit errors are among the top reasons for GST notices. Common problems include: Claiming ineligible ITC Vendor non-compliance Duplicate claims 4. GST Reconciliation Failures Mismatch between: Books of accounts GST returns E-way bills E-invoices …can trigger automated scrutiny. 5. E-Invoicing Non-Compliance Businesses crossing prescribed turnover thresholds must comply with e-invoicing regulations. Non-compliance can result in: Invalid invoices ITC denial Penalties Penalties & Risks of GST Non-Compliance Compliance Failure Possible Consequence Late filing Interest + penalties Incorrect ITC ITC reversal Under-reporting turnover GST notice E-invoice errors Compliance action Persistent non-compliance GST registration suspension GST Compliance Checklist for 2026 Monthly Tasks File GSTR-1 File GSTR-3B Reconcile ITC claims Quarterly Tasks Review vendor compliance Validate turnover reconciliation Annual Tasks Annual GST return filing Financial audit support Why Businesses Need Professional GST Support GST regulations continue evolving rapidly. Professional GST consultants help businesses: ✔ Reduce notice risks✔ Maintain filing accuracy✔ Optimize Input Tax Credit✔ Ensure audit readiness✔ Improve compliance efficiency This becomes especially important for: Startups SMEs Multi-state businesses E-commerce sellers Why CA Arihant Lodha is a Strong Compliance Partner CA Arihant Lodha offers: GST registration assistance End-to-end GST compliance support GST reconciliation & audit preparation Startup and SME-focused advisory Conclusion GST registration gets your business into the system. GST compliance keeps your business safe inside it. In 2026, the difference between these two concepts is no longer minor—it directly impacts: ✔ Financial stability✔ Tax efficiency✔ Compliance risk✔ Business reputation Businesses that treat GST strategically avoid unnecessary penalties and operational stress. CTA Need help with GST compliance, return filing, or GST notices? Consult CA Arihant Lodha for professional GST advisory and compliance services in Mumbai. FAQ SECTION 1. What is the difference between GST registration and GST compliance? GST registration is obtaining a GSTIN, while GST compliance involves ongoing filing, reconciliation, and reporting obligations. 2. Is GST registration enough for businesses? No. Businesses must continue complying through regular filings and tax payments. 3. What happens if GST returns are not filed? Late filing can lead to penalties, interest, notices, and even suspension of GST registration. 4. Why do businesses receive GST notices? Common reasons include mismatches, incorrect ITC claims, and delayed filings. 5. What is GST reconciliation? It is the process of matching invoices, GST returns, and financial records for accuracy. 6. Can GST non-compliance affect Input Tax Credit? Yes. Incorrect or non-compliant filings can result in ITC reversal or denial. Blog By : CA Arihant Lodha

Virtual CFO Services in Mumbai: Cost, Benefits & When Your Business Actually Needs One

A Virtual CFO provides strategic financial leadership without full-time cost Ideal for startups and SMEs scaling beyond basic accounting Costs range from ₹15,000 to ₹1,00,000+/month depending on scope Helps with cash flow, fundraising, compliance, and growth strategy Hiring at the right stage prevents financial chaos Introduction Most businesses don’t fail because of bad products—they fail because of poor financial decisions. In Mumbai’s competitive business environment, founders often rely on accountants for compliance—but lack strategic financial direction. That’s where Virtual CFO services come in. In 2026, businesses are increasingly shifting to outsourced CFO models to access high-level financial expertise without hiring a full-time executive. What is a Virtual CFO? 🤔 A Virtual CFO (Chief Financial Officer) is a financial expert who provides: Strategic financial planning Cash flow management Business forecasting Compliance oversight 👉 Unlike accountants, a CFO focuses on future growth, not just past records. What Does a Virtual CFO Actually Do? A Virtual CFO handles: Strategic Functions Financial planning & budgeting Business growth strategy Fundraising support Operational Functions Cash flow monitoring Expense optimization Profitability analysis Compliance & Risk Tax planning Regulatory compliance Financial reporting Key Benefits of Virtual CFO Services 🚀 1. Cost Efficiency No full-time salary burden Pay only for required expertise 2. Strategic Decision-Making Data-driven insights Growth-focused planning 3. Improved Cash Flow Management Predictive cash flow tracking Reduced financial stress 4. Investor & Funding Readiness Financial projections Due diligence preparation 5. Risk Reduction Compliance monitoring Early error detection Cost of Virtual CFO Services in Mumbai 💰 Service Level Monthly Cost Basic Advisory ₹15,000 – ₹30,000 Growth Stage Support ₹30,000 – ₹75,000 Advanced Strategic CFO ₹75,000 – ₹1,50,000+ 💡 Cost depends on: Business size Complexity Frequency of engagement Virtual CFO vs Full-Time CFO Factor Virtual CFO Full-Time CFO Cost Low Very High Flexibility High Low Expertise Access Wide Limited to one person Scalability Easy Difficult 👉 For startups & SMEs, Virtual CFO is the smarter choice. When Does Your Business Need a Virtual CFO? ⚠️ You should consider one if: Revenue crosses ₹50 lakh – ₹5 crore Cash flow issues are frequent You’re planning to raise funds Financial decisions feel unclear Compliance complexity increases Industries That Benefit the Most Startups & SaaS companies E-commerce brands Manufacturing SMEs Professional services firms Common Mistakes Without CFO Support Scaling without financial planning Poor cash flow management Overpaying taxes Lack of profitability insights Financial misreporting How to Choose the Right Virtual CFO in Mumbai Look for: ✅ Industry experience ✅ Strategic thinking ability ✅ Strong compliance knowledge ✅ Tech-driven reporting systems ✅ Transparent pricing Why CA Arihant Lodha is a Strong Choice Deep expertise in startups & SMEs End-to-end financial advisory Strong compliance + strategy integration Mumbai-focused business understanding Conclusion Financial clarity is no longer optional—it’s a competitive advantage. A Virtual CFO doesn’t just manage numbers—they shape business outcomes. In 2026, businesses that invest in financial strategy: ✔ Scale faster✔ Avoid costly mistakes✔ Attract investors CTA 🚀 Ready to scale your business with clarity?Consult CA Arihant Lodha for expert Virtual CFO services in Mumbai. FAQ SECTION 1. What does a virtual CFO do? Provides financial strategy, planning, and business insights. 2. How much does a virtual CFO cost in India? Typically ₹15,000 to ₹1,50,000+ per month. 3. When should a startup hire a CFO? When financial complexity increases or funding is planned. 4. Is a virtual CFO worth it? Yes, especially for growing businesses needing strategic insights. 5. What is the difference between CFO and accountant? Accountants manage records; CFOs manage strategy. Blog by : CA Arihant Lodha

Income Tax Filing Mistakes Business Owners in Mumbai Must Avoid This Financial Year

Tax filing errors can trigger penalties, notices, and audits Common mistakes include wrong income reporting and missed deductions Advance tax and GST mismatches are major red flags in 2026 A structured filing approach eliminates most risks CA guidance significantly improves accuracy and savings Introduction Income tax filing for business owners is no longer a routine compliance task—it’s a high-risk activity if done incorrectly. In 2026, the Income Tax Department uses AI-driven scrutiny systems, cross-verifying GST data, bank transactions, and reported income. Even small errors can trigger: Notices Penalties Scrutiny assessments This guide highlights the most critical income tax filing mistakes business owners in Mumbai must avoid—and how to fix them proactively. Why Tax Filing Errors Are Increasing in 2026 📊 Several structural changes have increased error detection: Automated reconciliation with GST returns Integration with banking and financial systems Real-time data validation Increased audit focus on SMEs 👉 Result: Mistakes that were previously ignored are now flagged instantly. Top Income Tax Filing Mistakes 1. Incorrect Income Reporting 🚨 Many businesses: Underreport revenue Exclude cash transactions Misclassify income 💡 This is the fastest way to trigger a tax notice. 2. Missing Eligible Deductions Common missed deductions: Business expenses Depreciation Rent & utility costs 👉 Missing deductions = higher tax liability unnecessarily 3. Choosing the Wrong ITR Form Using the incorrect ITR form leads to: Rejection of return Compliance complications 4. Ignoring Advance Tax Payments ⏱️ Businesses must pay advance tax in installments. Failure results in: Interest penalties under Sections 234B & 234C 5. Poor Record Keeping 📂 Missing invoices Unorganized expenses No audit trail 👉 Leads to compliance issues and weak defense during scrutiny. 6. GST & Income Tax Mismatch Mismatch between: GST turnover Income tax declared revenue This is a major red flag in 2026. Financial Impact of These Mistakes 💸 Mistake Possible Consequence Underreporting income Heavy penalties + scrutiny Late filing Interest + fines Incorrect deductions Higher tax liability GST mismatch Audit trigger Step-by-Step Checklist for Error-Free Filing ✅ Reconcile financial statements Match GST returns with income Verify deductions Select correct ITR form Pay advance tax on time Maintain proper documentation How to Correct Mistakes After Filing Made an error? Act fast: File a revised return before deadline Rectify errors via income tax portal Consult CA for major discrepancies How to Avoid Tax Notices in 2026 🚫 Maintain clean financial records Ensure GST & ITR consistency Avoid aggressive tax claims File returns on time Conduct periodic audits Why Hiring a CA is a Smart Move A professional CA: Identifies errors before submission Maximizes deductions legally Ensures compliance accuracy Represents you in case of notices Conclusion Tax filing mistakes are no longer minor errors—they are compliance risks with financial consequences. In a system driven by automation and data intelligence, accuracy is non-negotiable. The solution is simple: ✔ Stay organized✔ Follow structured processes✔ Work with experts CTA 🚀 Avoid costly tax mistakes this year.Consult CA Arihant Lodha for accurate, compliant, and optimized income tax filing in Mumbai. FAQ SECTION 1. What are common income tax filing mistakes? Incorrect income reporting, missed deductions, and wrong ITR forms are the most common. 2. Can tax filing mistakes lead to penalties? Yes. Errors can result in interest, fines, and scrutiny notices. 3. How to correct ITR mistakes? File a revised return before the deadline. 4. What is GST mismatch in tax filing? When GST turnover differs from income tax data. 5. How to avoid tax notices? Maintain accurate records, file on time, and ensure compliance. BLOG BY : CA Arihant Lodha

CA Firm in Mumbai for Startups: Complete Guide to Company Registration, GST & Compliance (2026)

Startups need CA support from day one to avoid costly mistakes Choose the right business structure (Pvt Ltd, LLP, OPC) GST registration is critical for most startups Compliance in 2026 is stricter due to automation A specialized CA firm ensures legal safety + growth readiness Introduction Starting a business in Mumbai is exciting—but compliance complexity can derail even the most promising startups. From company registration to GST filings and ongoing compliance, founders often underestimate the legal and financial groundwork required. The reality in 2026:👉 Compliance is no longer optional—it’s algorithmically enforced. This guide breaks down everything you need to know about working with a CA firm in Mumbai for startups, ensuring your business starts strong and scales safely. Why Startups Need a CA Firm Early 🚀 Many founders delay hiring a CA to “save cost.” That usually backfires. A startup-focused CA helps you: Choose the right legal structure Avoid tax inefficiencies Ensure compliance from day one Prepare for funding & due diligence 💡 Early mistakes in structure or GST can cost lakhs later. Types of Company Registration in India Choosing the correct structure is critical. Type Best For Key Benefit Private Limited Fundraising startups Scalability LLP Small businesses Lower compliance OPC Solo founders Full control 👉 For most startups aiming to scale, Private Limited Company is preferred. Step-by-Step Company Registration Process 🧾 Name Approval (RUN/DIR) Digital Signature Certificate (DSC) Director Identification Number (DIN) MOA & AOA Drafting Incorporation Filing (MCA) PAN & TAN Allotment ⏱️ Timeline: 7–12 working days (if documents are correct) GST Registration for Startups Is GST Mandatory? Yes, if: Turnover exceeds ₹40 lakh (₹20 lakh for services) You sell interstate You operate e-commerce GST Registration Process Apply on GST portal Submit business documents Verification & ARN generation Startup Compliance Requirements in 2026 📊 Compliance is stricter than ever. Key Requirements: GST returns (monthly/quarterly) TDS filings ROC compliance Income tax returns Accounting & bookkeeping Common Mistakes Startups Make ⚠️ Choosing wrong business structure Delaying GST registration Mixing personal & business finances Ignoring compliance deadlines DIY accounting without expertise How to Choose the Right CA Firm in Mumbai Look for: ✅ Startup Expertise ✅ End-to-End Services ✅ Transparent Pricing ✅ Technology-driven processes ✅ Advisory beyond compliance Cost Breakdown for Startup Services 💰 Service Estimated Cost Company Registration ₹8,000 – ₹25,000 GST Registration ₹2,000 – ₹5,000 Monthly Compliance ₹3,000 – ₹15,000 Why CA Arihant Lodha is Ideal for Startups Specialized in startup advisory End-to-end services (registration → compliance → tax planning) Mumbai-focused expertise Practical, business-first approach Conclusion Launching a startup is challenging—but compliance doesn’t have to be. The right CA firm acts not just as a service provider—but as a strategic partner. In 2026, startups that prioritize compliance early: ✔ Avoid penalties✔ Build investor trust✔ Scale faster CTA 🚀 Looking for a reliable CA firm in Mumbai for your startup?Connect with CA Arihant Lodha for expert guidance on registration, GST, and compliance. FAQ SECTION 1. Which CA firm is best for startups in Mumbai? A startup-focused CA firm offering end-to-end services is ideal. 2. Is GST required for startups? Yes, if turnover or business model meets GST criteria. 3. What is the cost of company registration? Typically between ₹8,000–₹25,000 depending on structure. 4. What compliances are required after registration? GST filing, ROC filing, tax returns, and accounting. 5. Can I register a company without a CA? Technically yes, but not recommended due to complexity. Blog by : CA Arihant Lodha

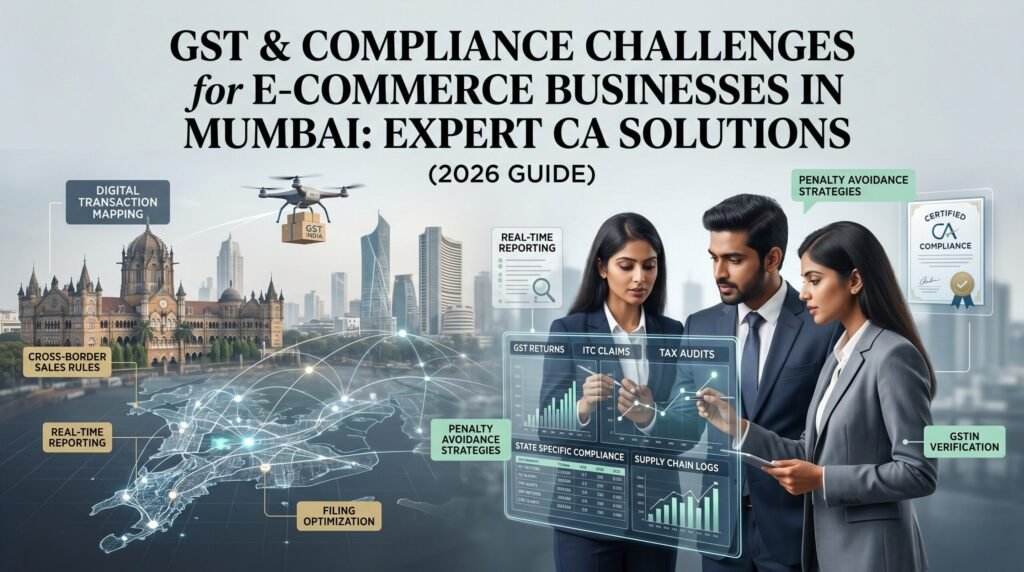

GST & Compliance Challenges for E-commerce Businesses in Mumbai: Expert CA Solutions (2026 Guide)

TL;DR GST is mandatory for most e-commerce sellers regardless of turnover TCS deduction by platforms complicates tax reconciliation Input tax credit mismatches are a major issue Monthly GST compliance is critical for avoiding penalties Expert CA support ensures accurate filings and tax optimization Why GST Compliance is Complex for E-commerce Unlike traditional businesses, e-commerce sellers operate across multiple states, platforms, and logistics networks. This creates: Multi-state GST liabilities Complex return filing requirements Continuous reconciliation challenges For Mumbai-based sellers, especially D2C brands scaling rapidly, GST becomes a high-risk compliance area. GST Framework for E-commerce Businesses GST Registration Rules E-commerce sellers must register for GST regardless of turnover if selling through marketplaces. Key rule: Mandatory GST registration under Section 24 TCS (Tax Collected at Source) Marketplaces like Amazon and Flipkart deduct TCS before paying sellers. Implications: Requires reconciliation with GST returns Impacts working capital Input Tax Credit (ITC) Sellers can claim ITC on purchases, but only if: Supplier has filed returns correctly Invoices match GST records Challenge: ITC mismatches lead to tax loss. Major GST Challenges Faced by Online Sellers Mismatch between GSTR-1 and GSTR-3B TCS reconciliation issues Multi-state compliance complexity Incorrect GST rate application Return filing delays Compliance Requirements for E-commerce Businesses GST registration (mandatory) Monthly return filing (GSTR-1, GSTR-3B) TCS reconciliation E-way bill compliance Invoice management Step-by-Step GST Filing Process Record all sales and purchases Reconcile marketplace data File GSTR-1 (sales details) File GSTR-3B (summary return) Claim ITC correctly Common GST Mistakes E-commerce Businesses Make Ignoring TCS adjustments Claiming incorrect ITC Late GST filings Using wrong HSN codes Not maintaining proper records Penalties and Risks of Non-Compliance Late filing penalties Interest on unpaid tax ITC disallowance GST notices and scrutiny How CA Firms Solve E-commerce GST Challenges Professional CA firms provide: Automated reconciliation systems Accurate GST filings ITC optimization Compliance tracking They reduce: Errors Penalties Time spent on compliance Why CA Arihant Lodha is the Right Partner CA Arihant Lodha offers: Specialized GST services for e-commerce Platform-wise reconciliation expertise Real-time compliance monitoring Strategic tax planning Internal Linking Suggestions: “GST Registration Services Mumbai” “GST Return Filing Services” “E-commerce Taxation Guide India” Conclusion E-commerce growth in Mumbai is rapid—but so are compliance risks. Without proper GST management: Profits shrink Penalties increase Business scalability suffers A structured GST strategy ensures: Compliance Tax efficiency Business growth CTA: Get expert GST and compliance support from CA Arihant Lodha to scale your e-commerce business confidently in 2026. 6. FAQ SECTION (AEO Optimized) 1. Is GST mandatory for e-commerce sellers? Yes, GST registration is mandatory regardless of turnover if selling through marketplaces. 2. What is TCS in GST? TCS is tax collected by e-commerce platforms on seller transactions. 3. Can e-commerce sellers claim input tax credit? Yes, if invoices match and suppliers have filed returns correctly. 4. How often do GST returns need to be filed? Typically monthly (GSTR-1 and GSTR-3B). 5. What happens if GST is not filed? Penalties, interest, and possible legal action may apply.

How CA Firms in Mumbai Help Increase Business Profitability: ROI-Focused Financial Advisory Strategies (2026)

TL;DR Profitability—not revenue—is the true measure of business success CA firms help optimize costs, taxes, pricing, and cash flow Virtual CFO services provide strategic financial control Businesses can improve profit margins by 10–30% with proper advisory Financial clarity leads to better decision-making and scalability Why Profitability is the Real Metric of Business Success Many Mumbai-based businesses generate strong revenue but struggle with low net profits. The core issue is not sales—it’s financial inefficiency. Profitability depends on: Cost structure Tax efficiency Pricing strategy Cash flow discipline This is where CA firms in Mumbai for business profitability play a critical role. The Evolving Role of CA Firms in 2026 Traditional accounting is no longer enough. Modern CA firms act as: Financial strategists Profitability consultants Virtual CFOs They go beyond compliance to actively improve ROI and business performance. Key Financial Advisory Strategies Used by CA Firms Cost Optimization & Expense Control Most businesses overspend without realizing it. CA-driven strategies include: Expense audits Vendor cost negotiation Eliminating non-performing expenses Impact: 5–15% cost reduction directly improves profits. Tax Planning & Optimization Poor tax planning reduces net income significantly. Strategies: Structuring income efficiently Utilizing deductions and exemptions Advance tax planning Result: Legal reduction in tax liability. Cash Flow Management Profit doesn’t guarantee liquidity. CA firms help: Track receivables and payables Optimize working capital Prevent cash crunch situations Pricing & Margin Optimization Incorrect pricing kills profitability. CA insights include: Break-even analysis Contribution margin calculation Product/service profitability tracking Virtual CFO Services: The Game Changer Virtual CFO services provide high-level financial expertise without full-time cost. Key functions: Financial planning & forecasting Budgeting and variance analysis Investor reporting Strategic decision support For SMEs in Mumbai, this is a high ROI service. Industry-Specific Profitability Strategies Manufacturing Reduce production wastage Optimize inventory cycles Real Estate Tax-efficient structuring Cash flow planning for projects E-commerce Optimize logistics costs Manage GST and pricing Professional Services Improve billing efficiency Control overhead costs Real Example: Profitability Transformation Case: A Mumbai-based SME with ₹2 crore revenue had only 5% net profit. Result: Profit margin increased to 15%. Common Profit-Killing Mistakes Businesses Make Ignoring financial reports Overstaffing or inefficient hiring Poor pricing strategy Lack of tax planning No cash flow monitoring How to Choose the Right CA Firm in Mumbai Look for: Financial advisory expertise (not just compliance) Experience across industries Ability to provide CFO-level insights Transparent pricing Proven track record Why CA Arihant Lodha is a Profitability Partner CA Arihant Lodha focuses on: ROI-driven financial strategies End-to-end business advisory Tax-efficient structuring Growth-focused financial planning Internal Linking Suggestions: “Virtual CFO Services in Mumbai” “Business Tax Planning Services” “Financial Advisory for SMEs” Conclusion Revenue growth without profitability is unsustainable. Businesses that succeed in 2026 are those that: Control costs Optimize taxes Manage cash flow Make data-driven decisions A strategic CA firm transforms your business into a profit-generating engine. CTA: Work with CA Arihant Lodha to unlock higher profitability and build a financially strong business in Mumbai. 6. FAQ SECTION 1. How can a CA help increase business profitability? By optimizing costs, reducing tax liability, improving pricing, and managing cash flow effectively. 2. What are financial advisory services? They include budgeting, forecasting, tax planning, and strategic financial decision-making support. 3. What is a virtual CFO? A virtual CFO provides high-level financial strategy without the cost of a full-time CFO. 4. How do businesses reduce tax legally? Through deductions, exemptions, and efficient income structuring. 5. How can I improve my business cash flow? By managing receivables, controlling expenses, and optimizing working capital.

Industry-Wise Audit & Compliance Requirements in Mumbai: A Complete Guide for SMEs & Corporates (2026)

TL;DR Multiple audits apply depending on turnover, structure, and industry Statutory audit is mandatory for all companies Tax audit applies beyond specified turnover limits Industry-specific compliance is often overlooked Non-compliance can lead to penalties, notices, and reputational damage Why Audit & Compliance Matter More Than Ever in 2026 Regulatory scrutiny in India has intensified significantly. With digital tracking, GST integration, and MCA monitoring, businesses in Mumbai face real-time compliance checks. For SMEs and corporates, compliance is no longer optional—it is a core business function. Types of Audits Applicable in India Statutory Audit Mandatory for all companies under the Companies Act. Key objectives: Verify financial statements Ensure legal compliance Build stakeholder trust Tax Audit Applicable under Section 44AB. Thresholds (2026): ₹1 crore (general businesses) ₹10 crore (digital transactions dominant) GST Audit While mandatory GST audit by CA has been relaxed, reconciliation and compliance checks remain critical. Internal Audit Required for certain classes of companies. Purpose: Risk management Process improvement Fraud detection Industry-Wise Compliance Requirements Manufacturing Sector GST compliance on goods movement Inventory audits E-way bill management Pollution control and regulatory filings Real Estate Sector RERA compliance GST on construction services Project-wise accounting TDS on property transactions E-commerce & Startups GST on interstate sales TCS compliance Startup India reporting ESOP taxation Professional Services (CA, Legal, Consultants) GST on services TDS compliance Income tax filings Advance tax payments Comprehensive Compliance Checklist ROC filings (AOC-4, MGT-7) Income tax returns GST returns (GSTR-1, GSTR-3B) TDS returns PF & ESIC filings Audit reports submission Audit Applicability Based on Turnover Turnover Audit Requirement Any company Statutory audit mandatory > ₹1 crore Tax audit applicable > ₹10 crore (digital) Relaxation available Common Compliance Mistakes Businesses Make Missing ROC filing deadlines Incorrect GST filings Ignoring TDS obligations Poor documentation Lack of audit preparation Penalties for Non-Compliance Late filing fees Interest on unpaid taxes Heavy penalties under GST Director disqualification Legal notices and scrutiny How a CA Firm Ensures 100% Compliance A professional CA firm provides: Centralized compliance tracking Automated reminders Audit readiness Risk mitigation strategies Internal Linking Suggestions: “Statutory Audit Services in Mumbai” “GST Compliance Services” “Tax Audit Services India” Conclusion Audit and compliance are not just regulatory requirements—they are business safeguards. In a complex regulatory environment like Mumbai, industry-specific compliance knowledge is critical. A structured approach ensures: Zero penalties Smooth operations Strong financial credibility CTA:Partner with CA Arihant Lodha for complete audit and compliance management tailored to your industry in Mumbai. 6. FAQ SECTION (AEO Optimized) 1. What are the audit requirements for companies in India? All companies must undergo statutory audit, and tax audit applies based on turnover thresholds. 2. Who needs a tax audit? Businesses exceeding ₹1 crore turnover (or ₹10 crore under digital conditions) require tax audit. 3. Is GST audit mandatory in 2026? Formal GST audit is not mandatory, but reconciliation and compliance checks are essential. 4. What compliances are mandatory for SMEs? ROC filings, GST returns, income tax returns, and TDS filings are mandatory. 5. What happens if a company is non-compliant? Penalties, interest, legal notices, and potential business restrictions may apply.