GST Notices 2026: Respond, Avoid Penalties

TL;DR GST Notices 2026 are rising in 2026 due to increased automation and data matching by the government. If you receive a notice, respond within the deadline, provide accurate documentation, and seek expert guidance. Ignoring notices can lead to penalties, interest, or legal action. Why GST Notices 2026 Are Increasing in 2026 The GST system has evolved significantly with: AI-based return matching Real-time invoice tracking Stronger compliance enforcement This means even minor mismatches trigger notices automatically. Key Insight:Most GST notices today are system-generated — not manually issued. Types of GST Notices You Must Know Understanding the type of notice is critical before responding. 1. GSTR-1 vs GSTR-3B Mismatch Occurs when sales reported differ from tax paid. Cause: Incorrect reporting Missed invoices 2. Input Tax Credit (ITC) Mismatch Triggered when: Supplier hasn’t filed returns ITC claimed is higher than eligible 3. Late Filing / Non-Filing Notices Issued when returns are delayed or not filed. 4. Scrutiny Notices Detailed examination of returns under GST law. Step-by-Step: How to Respond to a GST Notices 2026 Step 1: Read the Notice Carefully Identify: Notice type Section reference Deadline Step 2: Verify Data Check: GST returns Books of accounts Invoices Step 3: Identify the Issue Common issues: Mismatch Missing filings Incorrect ITC Step 4: Prepare Supporting Documents Invoices GST returns Reconciliation statements Step 5: Draft a Proper Reply Ensure: Clear explanation Supporting evidence Professional tone Step 6: Submit Response Online Via GST portal within deadline. GST Notice Reply Format (Practical Template) Subject: Reply to GST Notice [Reference No.] Dear Sir/Madam, We acknowledge receipt of the notice dated [date]. Upon review, we submit the following: Explanation of discrepancy Supporting documents attached Corrective action taken We request your kind consideration. Regards,[Business Name] Penalties: What Happens If You Ignore Notices Ignoring GST notices can result in: Penalty up to 10% of tax amount Interest charges Suspension of GST registration Legal proceedings How to Avoid GST Notices in Future 1. Monthly Reconciliation Match GSTR-1, GSTR-3B, and books regularly. 2. Accurate ITC Claims Avoid excess or ineligible claims. 3. Timely Filing Never delay GST returns. 4. Vendor Compliance Check Ensure suppliers file returns properly. 5. Use Automation Tools Reduce manual errors. Role of CA in GST Compliance A professional CA firm ensures: Error-free filings Timely compliance Proper notice handling Strategic tax planning Final Checklist Before submitting a GST reply: Verified all data Attached documents Checked deadlines Reviewed reply professionally Conclusion GST notices are not a threat — they are a signal of compliance gaps. Businesses that act quickly and correctly: Avoid penalties Maintain compliance Build credibility CTA: Facing a GST notice? Get expert assistance from CA Arihant Lodha handle notices, reduce penalties, and ensure complete compliance. 6. FAQ SECTION 1. What should I do if I receive a GST notice?Immediately review the notice, identify the issue, and respond within the deadline with proper documentation. 2. Can I ignore a GST notice?No. Ignoring can lead to penalties, interest, and legal action. 3. How to reply to GST notice online?Log in to the GST portal, navigate to notices, and submit your response with documents. 4. What is the penalty for GST notice?Penalty can be up to 10% of tax liability along with interest. 5. How to avoid GST notices?Maintain accurate records, reconcile returns monthly, and ensure timely filing. Blog By : CA Arihant Lodha

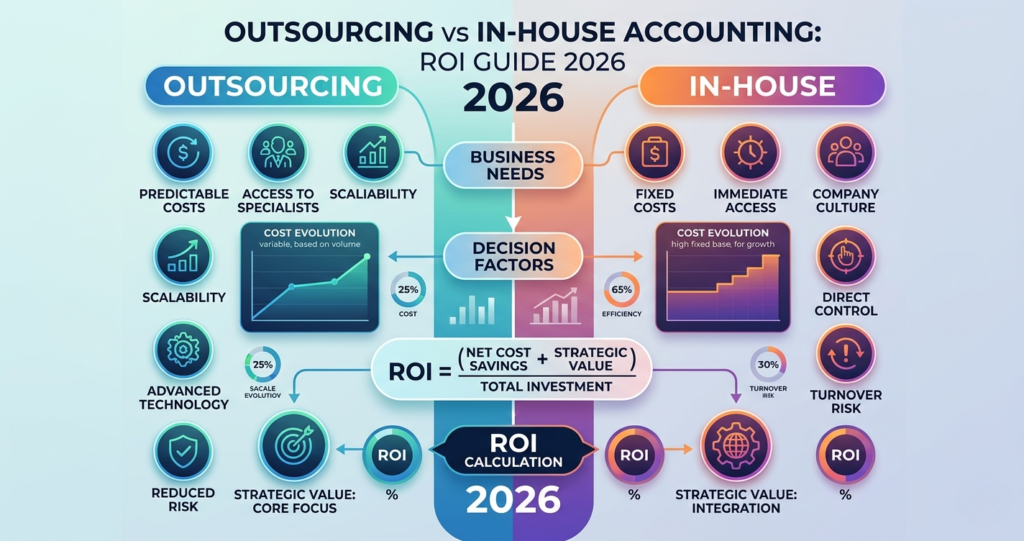

Outsourcing vs In-House Accounting: ROI Guide 2026

TL;DR Outsourced accounting delivers 30–50% cost savings, better scalability, and higher compliance efficiency for most startups and SMEs. In-house teams make sense only for large enterprises with complex, real-time financial needs. Why This Decision Matters in 2026 Accounting is no longer just bookkeeping. In 2026, it directly impacts: Profit margins Compliance risk Fundraising readiness Business scalability With rising salaries, compliance complexity, and tech adoption, choosing the wrong model can cost businesses lakhs annually. What is In-House Accounting? An in-house accounting team involves hiring: Accountants Finance managers Compliance specialists Typical Setup: 1 Accountant: ₹3–6 LPA 1 Senior Accountant: ₹6–12 LPA Tools & software: ₹1–2 LPA Total Annual Cost: ₹10–20+ lakhs What is Accounting Outsourcing? Outsourcing means delegating accounting functions to a CA firm or specialized service provider. Services Include: Bookkeeping GST filing TDS & payroll Financial reporting Compliance management Typical Cost: ₹1–5 lakhs annually (depending on scale) Cost Comparison: Real Numbers Factor In-House Team Outsourcing Salary Cost High None Software Cost High Included Training Cost Ongoing Zero Scalability Cost Expensive Flexible Total Annual Cost ₹10–20L ₹1–5L Insight:Outsourcing reduces accounting costs by 50–80%. ROI Breakdown: Outsourcing vs In-House ROI is not just cost — it’s value delivered. Outsourcing ROI Drivers: Lower operational cost Access to expert CAs Reduced compliance penalties Faster reporting In-House ROI Drivers: Real-time control Internal coordination Custom processes Verdict:For 90% of SMEs, outsourcing delivers higher ROI due to cost efficiency + expertise. Scalability & Flexibility Analysis In-House Limitations: Hiring delays Fixed cost structure Difficult to scale up/down Outsourcing Advantages: Pay-as-you-grow model Instant scalability No hiring dependency Compliance & Risk Management Compliance errors can cost businesses heavily. Outsourcing Advantage: Dedicated compliance experts Up-to-date with tax laws Reduced penalties In-House Risk: Knowledge gaps Dependency on individuals Technology & Automation Advantage Outsourcing firms use: Cloud accounting tools Automation workflows Real-time dashboards In-house teams often lag due to: Budget constraints Resistance to change When In-House Makes Sense Choose in-house if: Revenue > ₹50 Cr Complex financial operations Need daily financial control Large internal teams When Outsourcing Wins Outsourcing is ideal if: Startup or SME Revenue < ₹50 Cr Need cost optimization Limited finance expertise Hybrid Model (Best of Both Worlds) Many businesses adopt: 1 internal finance manager Outsourced accounting team This ensures: Strategic control Operational efficiency Final Verdict For most Indian businesses in 2026: Outsourcing = Higher ROI In-house = Higher control The smartest companies don’t choose one blindly — they choose based on scale and strategy. Conclusion Accounting is a strategic function, not just a compliance requirement. Businesses that outsource smartly gain: Cost efficiency Expert insights Better compliance Faster growth CTA:Looking to reduce accounting costs and improve financial efficiency? Partner with CA Arihant Lodha & Associates for expert outsourced accounting solutions tailored to your business. 6. FAQ SECTION 1. Is outsourcing accounting cheaper than in-house?Yes. Outsourcing can reduce costs by 50–80% compared to hiring a full in-house team. 2. Is outsourced accounting safe?Yes, if handled by a professional CA firm with proper data security and compliance systems. 3. When should I hire an in-house accountant?When your business requires real-time financial decision-making and has complex operations. 4. What is the ROI of outsourced accounting?Higher ROI due to lower costs, expert handling, and reduced compliance risks. 5. Can startups rely fully on outsourcing?Yes, most startups operate efficiently with outsourced accounting until they scale. Blog By : CA Arihant & Lodha