Why Businesses Receive Income Tax Notices and How to Prevent Them Legally

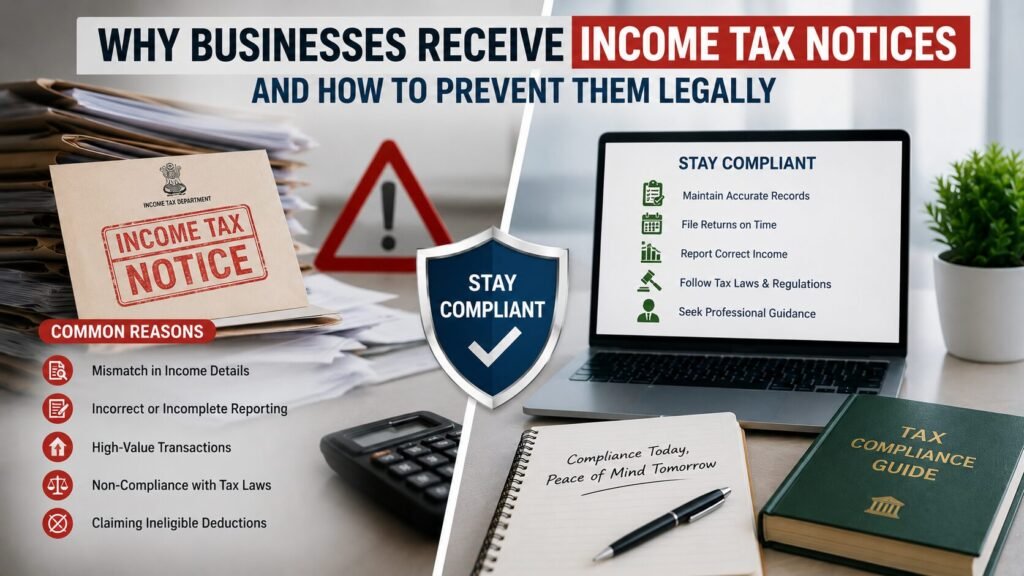

TL;DR Businesses usually receive an income tax notice because the Income Tax Department finds a mismatch, missing disclosure, delayed filing, high-value transaction, incorrect claim, or unexplained entry in the return. Common triggers include AIS mismatch, Form 26AS mismatch, TDS differences, GST turnover mismatch, high-value transactions, incorrect income reporting, excessive deductions, defective returns, and tax audit issues. Most notices can be prevented legally through accurate bookkeeping, timely filing, proper reconciliation, supporting documentation, tax planning, and professional review before filing returns. Why Income Tax Notices Are Becoming More Common Income tax compliance in India has become heavily data-driven. The Income Tax Department now receives financial information from multiple reporting sources such as banks, stock exchanges, mutual funds, property registrars, GST records, TDS statements, TCS reports, and other specified financial transaction reports. This data appears in documents such as: AIS TIS Form 26AS TDS statements TCS statements GST returns SFT reports Bank transaction reports When the income tax return does not match the data available with the department, the system can flag the case for review. For businesses, this means one thing clearly: Tax filing is no longer only about entering numbers in the return. It is about making sure every reported figure matches supporting records across multiple systems. What Is an Income Tax Notice? An income tax notice is an official communication from the Income Tax Department asking the taxpayer to explain, correct, verify, or respond to a specific issue. A notice may be issued for: Mismatch in income Missing disclosure Defective return Scrutiny assessment High-value transaction TDS mismatch Tax demand Non-filing of return Reassessment Refund adjustment Clarification of records Not every notice means tax fraud or penalty. Many notices are triggered by data mismatch, reporting differences, or clerical errors. However, ignoring a notice can make the matter serious. Common Reasons Businesses Receive Income Tax Notices 1. AIS, TIS and Form 26AS Mismatches AIS, TIS and Form 26AS are important tax information records. They may contain details of: Interest income TDS deducted TCS collected Sale of securities Mutual fund transactions Property transactions Dividend income Business receipts High-value transactions If the income reported in the ITR does not match these records, a notice may be triggered. Example A business reports ₹85 lakh turnover in its ITR, but the information available in AIS indicates receipts of ₹95 lakh through reported transactions. This difference can create a mismatch and lead to a notice. Prevention Before filing the return: Download AIS Review TIS Check Form 26AS Match with books of accounts Submit AIS feedback where data is incorrect Keep supporting documents ready 2. TDS and TCS Differences TDS and TCS mismatches are common in business tax filing. Reasons include: Deductor filed incorrect TDS return PAN mismatch TDS not reflected in Form 26AS Income booked in a different year Wrong section used by deductor TDS claimed without corresponding income TCS shown but transaction not disclosed Prevention Reconcile TDS and TCS with: Books of accounts Form 26AS AIS Customer/vendor confirmations Tax credit statements Never claim tax credit without checking whether the related income has also been reported correctly. 3. High-Value Transactions High-value transactions are reported to the Income Tax Department by banks, registrars, mutual funds, credit card companies, and other reporting entities. Examples may include: Large cash deposits Property purchases Sale of immovable property High credit card payments Large investments Share and mutual fund transactions Foreign remittances Fixed deposit transactions If these transactions are not properly explained in the ITR or books, a notice may follow. Prevention Maintain proper source documentation for every major transaction. Examples: Bank statements Sale deeds Investment statements Loan agreements Gift deeds Board approvals Capital introduction records Customer receipts The goal is not to avoid legitimate transactions. The goal is to ensure they are properly reported and explainable. 4. GST Turnover vs Income Tax Return Mismatch For businesses registered under GST, turnover reported in GST returns may be compared with income reported in the income tax return. Mismatch may arise due to: Different reporting periods Credit notes Debit notes Advances Exempt supplies Export turnover Accounting errors Unreconciled sales Incorrect GST reporting Example GST returns show outward taxable supplies of ₹1.8 crore, but the business reports gross receipts of ₹1.55 crore in the ITR without proper reconciliation. This can lead to scrutiny. Prevention Prepare a GST-to-ITR turnover reconciliation before filing income tax returns. 5. Incorrect Income Reporting Businesses may receive notices when income is underreported, misclassified, or omitted. Common issues include: Business income shown as other income Interest income not reported Rental income missed Capital gains not disclosed Foreign income omitted Professional receipts not fully reported Commission income ignored Cash sales not recorded Prevention Create an income classification review before return filing. Every receipt should be mapped to the correct tax head. 6. Excessive or Unsupported Expense Claims The department may question expenses that appear unusual, excessive, unsupported, or unrelated to business. Commonly reviewed expenses include: Travel Consultancy charges Commission payments Advertisement expenses Repairs and maintenance Cash expenses Related-party payments Professional fees Business promotion expenses Prevention Maintain: Bills Agreements Payment proofs Work completion evidence GST invoices TDS compliance records Board approvals where required Expenses should be genuine, business-related, and properly documented. 7. Delayed or Non-Filing of Income Tax Return Late filing or non-filing can trigger notices. Businesses may be flagged if: Tax has been deducted but return is not filed GST turnover exists but ITR is missing High-value transactions exist but no return is filed Previous years were filed but current year is missing Advance tax was paid but return is not filed Prevention Maintain a compliance calendar. Track: ITR due dates Tax audit due dates Advance tax dates TDS return dates GST return dates ROC filing dates 8. Defective Return Filing A return may be treated as defective when key information is incomplete, inconsistent, or technically incorrect. Common causes include: Wrong ITR form Missing balance sheet details Missing P&L details Incorrect audit information Mismatch in tax paid Incomplete schedules Wrong business code Missing partner/director details Prevention Review the return carefully before filing. A

LLP vs Private Limited Company: A Complete Decision Guide for Entrepreneurs

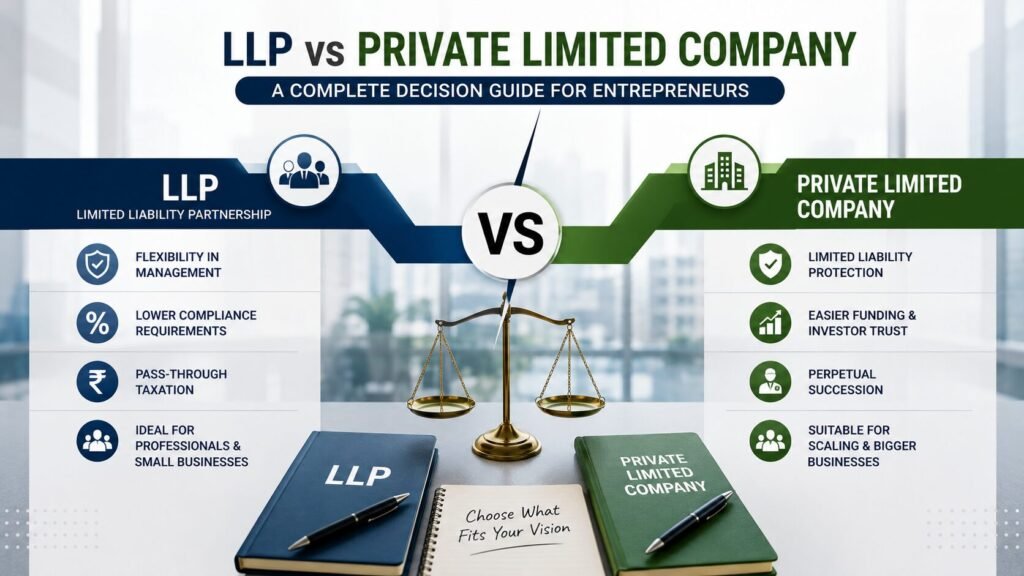

TL;DR Choosing between an LLP and a Private Limited Company depends on your business model, funding plans, compliance capacity, ownership structure, and long-term growth vision. An LLP is generally suitable for professionals, consultants, service businesses, and closely held ventures that want limited liability with relatively simpler compliance. A Private Limited Company is better suited for startups, scalable businesses, investor-backed ventures, and companies planning to raise funds, issue shares, build ESOPs, or expand aggressively. For most entrepreneurs, the right question is not “Which structure is cheaper?” The better question is: Which structure supports your business goals for the next 3–5 years? Why Choosing the Right Business Structure Matters Business registration is one of the first major decisions an entrepreneur makes. It affects taxation, compliance, investor confidence, ownership rights, liability, fundraising, governance, and future expansion. Many founders choose an entity based only on reg istration cost. That is a mistake. A structure that looks affordable today may become restrictive lat er. For example, an LLP may work well for a consulting firm, but it may not be ideal for a startup planning to raise venture capital. Similarly, a Private Limited Company may offer strong credibility but also comes with higher compliance responsibilities. Entrepreneurs should choose the structure based on: Business model Number of founders Funding plans Expected revenue scale Compliance capacity Tax planning Exit strategy Investor expectations Long-term expansion goals This guide explains the difference between LLP vs Private Limited Company in practical terms. What Is an LLP? LLP stands for Limited Liability Partnership. It combines features of a partnership firm and a company. Partners can manage the business directly while enjoying limited liability protection. In an LLP, the liability of partners is generally limited to their agreed contribution. This means personal assets are usually protected against business liabilities, subject to fraud, negligence, or personal guarantees. LLPs are commonly preferred by: Consultants Chartered accountants Lawyers Architects Small service businesses Family-run ventures Professional firms Agencies Closely held businesses An LLP is flexible, relatively easier to manage, and suitable where external equity funding is not a major goal. What Is a Private Limited Company? A Private Limited Company is a separate legal entity registered under the Companies Act, 2013. It has shareholders, directors, share capital, board governance, statutory records, and formal compliance requirements. Private Limited Companies are commonly preferred by: Startups Technology companies D2C brands SaaS businesses Manufacturing companies Fundraising-focused ventures Scalable service businesses Companies planning ESOPs Businesses targeting institutional investors A Private Limited Company is usually seen as more structured, scalable, and investor-friendly. LLP vs Private Limited Company: Quick Comparison Factor LLP Private Limited Company Governing Law LLP Act, 2008 Companies Act, 2013 Owners Partners Shareholders Management Designated Partners Directors Liability Limited Limited Compliance Moderate Higher Investor Funding Limited suitability Highly suitable ESOPs Not ideal Suitable Ownership Transfer Less flexible More flexible Credibility Good Stronger for scaling Best For Professionals, consultants, SMEs Startups, scalable companies, investor-backed ventures Key Differences Entrepreneurs Should Understand 1. Ownership Structure In an LLP, ownership rests with partners. Their rights, profit-sharing ratio, capital contribution, and responsibilities are governed by the LLP agreement. In a Private Limited Company, ownership is represented through shares. Shareholders own the company, while directors manage operations. This difference becomes important when: New investors enter Founders exit Ownership changes ESOPs are issued Shares are transferred Valuation is negotiated A Private Limited Company offers a clearer ownership structure for investor-backed businesses. 2. Liability Protection Both LLP and Private Limited Company provide limited liability protection. However, limited liability does not mean unlimited protection. Founders or partners may still become personally liable in cases involving: Fraud Misrepresentation Personal guarantees Non-compliance Wrongful conduct Statutory defaults For normal business risks, both structures protect personal assets better than a traditional partnership or proprietorship. 3. Compliance Burden Compliance is one of the biggest practical differences. An LLP generally has fewer annual compliance requirements compared to a Private Limited Company. Typical LLP compliances include: Annual return filing Statement of accounts and solvency Income tax return Audit, if applicable Partner-related filings when changes occur A Private Limited Company generally requires: Annual ROC filings Board meetings Shareholder meetings Statutory registers Director KYC Financial statements Auditor appointment Income tax filing GST and TDS compliance, if applicable Event-based MCA filings If simplicity is the main priority, LLP may be better. If scalability and investor readiness matter more, Private Limited Company is usually stronger. 4. Taxation Taxation should not be viewed only from the rate perspective. The overall tax impact depends on profits, withdrawals, remuneration, dividends, business model, and future plans. An LLP is taxed as a firm. Partners may receive remuneration or profit share depending on the LLP agreement and tax provisions. A Private Limited Company pays corporate tax, and distribution of profits to shareholders may have additional tax implications depending on the method of extraction. Entrepreneurs should review: Expected profits Founder remuneration Dividend plans Reinvestment requirements Investor entry Tax audit applicability GST and TDS obligations A CA should evaluate the tax impact before finalising the structure. 5. Funding and Investment This is where Private Limited Company usually has a clear advantage. Most angel investors, venture capital firms, private equity investors, and institutional investors prefer Private Limited Companies because shares can be issued, transferred, valued, and documented more easily. A Private Limited Company is better suited for: Angel funding Venture capital ESOPs Convertible instruments Share transfers Strategic investment Future acquisition An LLP is not the preferred structure for equity fundraising. If your business plans to raise funds, issue ESOPs, or bring in investors, Private Limited Company is usually the better choice. 6. Scalability A Private Limited Company generally offers better scalability because it has a formal governance structure. It is suitable for businesses planning: Multiple founders Senior leadership hiring Investor reporting Large contracts Expansion to multiple states Bank funding Institutional partnerships Employee stock options Merger or acquisition opportunities LLPs can also grow, but they are usually better suited for businesses where ownership remains closely held. 7. Credibility A Private Limited Company often carries stronger credibility with